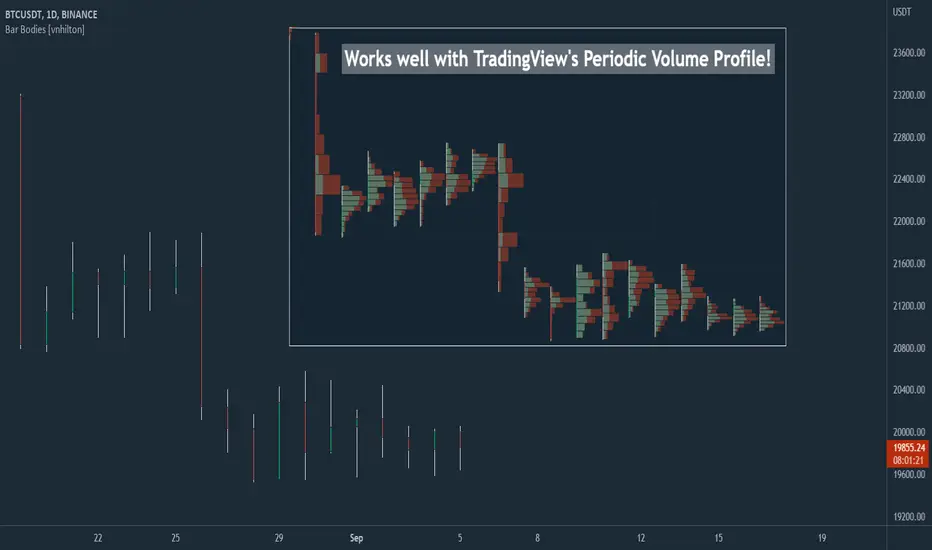

Volume Footprint POC for Every CandleCalculating and plotting the Point of Control (POC) for every candle on a volume footprint chart can provide valuable insights for traders. Here are some interpretations and uses of this information:

1. Identify Key Price Levels

Highest Traded Volume: The POC represents the price level with the highest traded volume for each candle. This level often acts as a significant support or resistance level.

Confluence Zones: When multiple POCs align at similar price levels over several candles, it indicates strong support or resistance zones.

2. Gauge Market Sentiment

Buyer and Seller Activity: High volume at certain price levels can indicate where buyers and sellers are most active. A rising POC suggests stronger buying activity, while a falling POC suggests stronger selling activity.

Volume Profile: Analyzing the volume profile helps in understanding the distribution of traded volume across different price levels, providing insights into market sentiment and potential reversals.

3. Spot Trends and Reversals

Trend Continuation: Consistent upward or downward shifts in POC levels can indicate a trend continuation. Traders can use this information to stay in trending positions.

Reversal Signals: A sudden change in the POC direction may signal a potential reversal. This can be used to take profits or enter new positions.

4. Intraday Trading Strategies

Short-Term Trading: Intraday traders can use the POC to make informed decisions on entry and exit points. For example, buying near the POC during an uptrend or selling near the POC during a downtrend.

Scalping Opportunities: High-frequency traders can use shifts in the POC to scalp small profits from price movements around these key levels.

5. Volume-Based Indicators

Confirmation of Other Indicators: The POC can be used in conjunction with other technical indicators (e.g., moving averages, RSI) to confirm signals and improve trading accuracy.

Support and Resistance: Combining the POC with traditional support and resistance levels can provide a more comprehensive view of the market dynamics.

In summary, the Point of Control (POC) is a valuable tool for traders to understand market behavior, identify key levels, and make more informed trading decisions. If you have specific questions or need further details on how to use this information in your trading strategy, feel free to ask! 😊

Cari skrip untuk "volume profile"

BTCUSD BOS & Liquidity MapBTCUSD is trading inside a high‑volume range after a clear series of Breaks of Structure (BOS) from the recent distribution zone into the current demand area. This chart highlights the key liquidity sweep, consolidation blocks and volume clusters that are likely to drive the next impulsive move.

Structure: Market shifted from a strong bullish leg into a clean bearish redistribution, confirmed by multiple BOS signals on the higher‑timeframe structure.

Liquidity: Price swept resting liquidity below prior lows and is now holding above the marked support band (89,270 – 88,300), suggesting absorption by buyers rather than continuation selling.

Volume profile: Visible Volume Profile shows heavy participation at the current range, reinforcing this zone as a potential accumulation area before a directional break.

Key levels:

Resistance zone: 97,950 – 98,300 (major supply and previous distribution ceiling).

Support zone: 89,270 – 88,300 (key demand and liquidity grab area).

Idea: As long as price holds above the support band, a reactive bullish leg back toward the resistance zone remains on the table. A clean break and acceptance below support would invalidate the bullish bias and open room for a deeper downside continuation.

This chart is for educational purposes only and not financial advice. Use it as a framework for your own entries, confirmations and risk management on BTCUSD.

Multy Dynamic POCThis script displays up to 4 independent Point of Control (POC) levels based on volume profile logic.

📌 Each POC can be configured individually:

Period options: Daily (D), Weekly (W), Monthly (M), or BARS (rolling bar window).

Dynamic recalculation when the period changes (e.g., new day/week/month or custom bar count).

Price-anchored lines for each POC level that scale correctly with the chart.

Customizable line color and thickness.

🔍 How it works:

For each active POC line, the script builds a simple volume distribution based on the candle’s average price (hl2) and volume.

The price range is split into 100 buckets. The one with the highest accumulated volume is selected as the Point of Control (POC).

In BARS mode, POC is recalculated every N bars. In D/W/M modes, it resets exactly at the beginning of a new period (according to TradingView’s time() function).

✅ Useful for:

Traders applying volume profile analysis without needing the full built-in volume profile tool.

Spotting dynamic high-volume zones in trends or ranges.

Strategy development or confirmation around high-interest price levels.

_______________________________________________________________________________

Данный индикатор отображает до 4 независимых уровней Point of Control (POC), рассчитанных по объёмам.

📌 Каждый POC можно настраивать отдельно:

Периоды: День (D), Неделя (W), Месяц (M) или BARS (скользящее окно по количеству баров).

Автоматический пересчёт при смене периода (например, новый день, неделя или месяц).

Линии POC привязаны к цене и масштабируются вместе с графиком.

Настраиваемый цвет и толщина линий.

🔍 Как работает:

Для каждой активной линии POC создаётся объёмное распределение: берется средняя цена свечи (hl2) и объем.

Диапазон цен делится на 100 уровней. Тот, где накоплено больше всего объёма, и есть POC.

В режиме BARS уровень пересчитывается каждые N баров. В режимах D/W/M — строго в начале нового периода.

✅ Подходит для:

Трейдеров, использующих объёмный анализ, но не имеющих платной подписки на Volume Profile.

Поиска уровней интереса и подтверждения сигналов.

Разработки стратегий с опорой на объём.

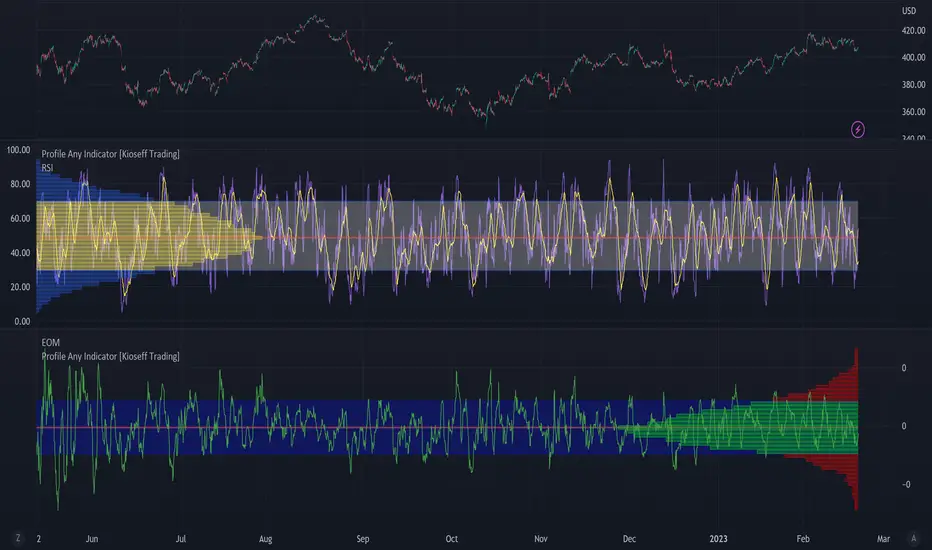

Profile Any Indicator [Kioseff Trading]Create a visible-range profile for almost any indicator!

Hello!

This script "Profile Any Indicator" allows you to create a visible-range profile for *almost* any indicator hosted on TradingView.

Therefore, the only requirement:

1. Indicator must have a retrievable plot value.

Should your indicator have a retrievable plot value (most indicators do), you can use this script to create a visible-range profile of its values!

Consequently, the profile's always oriented to the left-most or right-most side of your chart - updating as you scroll left or right.

The image above shows me using the indicator to create a profile for MACD. I am largely zoomed out and the profile has adjusted to chart orientation.

Let's zoom in and see what happens!

Voila!

The indicator adjusted to my chart positioning and created a new visible-range profile! No manual adjustments are required (:

Instructions

1. Load the indicator you'd like to profile on the chart.

The image above shows me applying the OBV indicator to the chart. Additionally, the "Profile Any Indicator" script is also loaded on the chart, instructing me to add an indicator to its settings.

2. From the settings for "Profile Any indicator", locate the "Indicator" setting and select the indicator you would like to profile.

The image above shows me selecting the OBV indicator in the settings for "Profile Any Indicator".

Once steps 1 and 2 are complete you'll have a visible-range profile for the selected indicator on your chart!

The image above shows the completion of the process.

3. Merge the indicator pane or select to plot the selected indicator in the current pane.

From here, you can select to plot the value of the selected indicator in the current pane or merge the selected indicator's pane (which must stay on the chart) with the pane designated to the "Profile Any Indicator" script.

The image above shows the two panes merged.

The image above shows the two panes separate. Alternatively, in the settings for "Profile Any Indicator", I selected to plot OBV in its pane.

You can select to populate the visible-range profile on the right of the chart!

Additionally, you can modify the POC line, value area %, and, essentially, any parameter you'd find for a volume-profile-like indicator!

Thanks for checking this out (:

Point of Control [BigBeluga]🔵 OVERVIEW

Point of Control identifies the exact price level with the highest traded volume over a selected lookback period.

This level—called the Point of Control (PoC) —marks where the greatest market participation occurred, representing a zone of highest volume.

The indicator helps traders visualize dominant volume concentrations, fair-value levels, and structural balance within recent price action.

🔵 CONCEPTS

Point of Control (PoC) — The single price level within the defined lookback range that has accumulated the most traded volume.

Volume Distribution Bins — The price range is divided into 25 equal bins, and volume is aggregated per bin to locate the maximum concentration.

Range Boundaries — The highest and lowest price within the lookback window are used to form the upper and lower reference limits.

PoC Channel — Optional upper and lower bands plotted around the main PoC to visualize a fair-value corridor.

Volume Intensity Mapping — Candle color dynamically shifts based on the candle’s position relative to the PoC channel, showing whether price is balanced or trending away from high-volume levels.

🔵 FEATURES

Configurable Lookback Range — Adjust how many bars (10–400) are used for calculating the PoC.

Precise PoC Calculation — Volume aggregation across 25 bins to identify the exact volume peak.

Dynamic Channel Visualization — PoC bands above and below the central level to indicate equilibrium tolerance.

Adaptive Candle Coloring —

- Neutral → price inside PoC channel. Gray

- Bullish → price above PoC channel. Blue 🔵

- Bearish → price below PoC channel. Orange 🟠

Automatic Volume Labeling — Displays total volume at the active PoC level for quick reference.

Directional Indicators — 🔵 or 🟠 markers appear when price shifts above or below the PoC channel.

Range Visualization — Plots the highest and lowest points of the active lookback window for contextual awareness.

Live Updating Logic — PoC recalculates automatically every 15 bars for efficient chart performance and accuracy.

🔵 HOW TO USE

Volume Anchoring — Use PoC as a reference for where the majority of volume occurred; price often reacts to or consolidates around this level.

Trend Confirmation — Sustained price movement away from PoC channel may signal developing directional imbalance.

Value Tracking — Watch the shifting of PoC across time to identify where fair value migrates during market evolution.

Equilibrium Mapping — When price hovers around PoC, the market is balanced; when it departs, a new value zone may form.

Combine With Volume Profiles — Use alongside profile tools for higher-resolution analysis of institutional activity.

🔵 CONCLUSION

Point of Control provides a pure, volume-centric view of market balance by pinpointing where most transactions occurred within any chosen range.

It delivers a clean and efficient visualization of fair value zones—helping traders track the heartbeat of market participation, recognize dominant liquidity areas, and stay aligned with where true market interest resides.

Statistcal Daily Profile & Ranges# Statistical Daily Profile & Ranges - TradingView Publication Guide

## Overview

The **Statistical Daily Profile & Ranges** indicator is a comprehensive tool designed to analyze intraday session behavior and daily range characteristics. It combines Average Daily Range (ADR) projection levels with detailed session-by-session statistics and probability-based trading insights derived from historical price action patterns.

## What This Indicator Does

This indicator provides traders with three core analytical components:

1. **ADR Projection Levels** - Dynamic support/resistance levels based on historical daily ranges

2. **Session Range Analysis** - Visual boxes and statistical breakdowns for four key trading sessions

3. **Dynamic Probability Display** - Real-time probability statistics based on overnight session relationships

## How It Works

### Average Daily Range (ADR) Calculation

The indicator calculates the average daily range over a user-defined lookback period (default: 10 days) and projects this range from each day's opening price. This creates two key levels:

- **ADR High**: Opening price + average daily range

- **ADR Low**: Opening price - average daily range

- **ADR Median**: The opening price (middle of the projected range)

These levels are recalculated at the start of each trading day and extend forward, providing dynamic support and resistance zones based on recent volatility characteristics.

### Session Tracking & Statistics

The indicator monitors four distinct trading sessions (times in Eastern Time):

1. **Asia Session** (8:00 PM - 2:00 AM)

2. **London Session** (2:00 AM - 8:00 AM)

3. **NY Open** (8:00 AM - 9:00 AM)

4. **NY Initial Balance** (9:30 AM - 10:30 AM)

For each session, the indicator:

- Draws a colored box showing the session's high-to-low range

- Tracks the opening price, high, and low

- Stores historical data for statistical analysis

- Calculates average ranges by day of week (Monday through Friday)

The session statistics are displayed in a customizable table showing average point ranges for each session across different weekdays, helping traders identify which sessions and days typically produce the most movement.

### Dynamic Probability System

The indicator analyzes the relationship between the Asia and London sessions to determine the current market setup. After the London session closes, it automatically detects one of four possible conditions:

**1. London Engulfs Asia**

- London session breaks both above Asia's high AND below Asia's low

- This indicates strong momentum during the European session

- Most common occurrence pattern

**2. Asia Engulfs London**

- Asia session range completely contains the London session range

- Indicates consolidation during London hours

- Relatively rare pattern (occurs approximately 5.36% of the time)

**3. London Partially Engulfs Upwards**

- London breaks above Asia's high but stays above Asia's low

- Suggests bullish momentum continuation from Asia into London

**4. London Partially Engulfs Downwards**

- London breaks below Asia's low but stays below Asia's high

- Suggests bearish momentum continuation from Asia into London

Once a condition is detected, the indicator displays a probability table showing historically observed outcomes for that specific setup, including:

- Probability of NY session taking out key levels (Asia high/low, London high/low)

- Probability of NY session engulfing the entire overnight range

- Directional bias for NY Cash session (9:30 AM - 4:00 PM)

## How to Use This Indicator

### Initial Setup

1. Add the indicator to your chart (works on any intraday timeframe below Daily)

2. Adjust the **ADR Days** setting (default: 10) to control the lookback period for range calculation

3. Adjust the **Session Lookback Days** setting (default: 50) to determine how much historical data feeds the statistics tables

### Reading the ADR Levels

- Use the **ADR High** and **ADR Low** lines as potential profit targets or areas where price may encounter resistance

- The **ADR Median** line represents the opening price and can act as a pivot point for intraday directional bias

- If price reaches the ADR High early in the session, it suggests strong bullish momentum; conversely for ADR Low

- These levels adapt daily based on recent volatility, making them more responsive than static levels

### Interpreting Session Boxes

- **Session boxes** visually highlight when each trading session is active and its price range

- Larger boxes indicate higher volatility during that session

- Compare current session ranges to the statistical averages shown in the table

- Sessions that are unusually quiet or active relative to historical averages may signal compression or expansion

### Using the Session Statistics Table

- The table shows average point ranges for each session broken down by weekday

- Identify which sessions typically produce the most movement on specific days

- For example, if London on Thursdays averages 40 points while Mondays average 25 points, you can adjust position sizing or expectations accordingly

- The **Total** column shows the overall average across all days

- Sample sizes (shown in brackets if enabled) indicate data reliability

### Trading with the Probability Table

The probability table updates dynamically after the London session closes and shows statistically probable outcomes based on 12 years of NQ futures data.

**Important Limitations:**

- **These probabilities are derived from NQ (Nasdaq E-mini futures) data only**

- **Do NOT apply these probability statistics to other instruments** (ES, stocks, forex, etc.)

- The probabilities represent historical frequencies, not guarantees

- Always combine with your own analysis, risk management, and market context

**How to Apply the Probabilities:**

When **London Engulfs Asia**:

- Watch for NY session to take out London's extremes (72.33% probability for high, 71.12% for low)

- Slight bullish bias in NY Cash session (54.80% vs 45.20%)

- Lower probability of complete overnight engulfment (44.13%)

When **Asia Engulfs London** (rare - 5.36% occurrence):

- Higher probability NY takes Asia's high (75.86%)

- Moderately high probability NY takes Asia's low (65.52%)

- Slight increase in bullish bias (58.42% vs 41.58%)

- Recognize this as an unusual setup

When **London Partially Engulfs Upwards**:

- Very high probability NY takes London high (81.51%)

- Strong probability NY takes London low (64.45%)

- Moderate probability NY takes Asian low (53.16%)

- Slight bullish bias (55.52%)

When **London Partially Engulfs Downwards**:

- Very high probability NY takes London low (75.29%)

- Strong probability NY takes London high (68.80%)

- Moderate probability NY takes Asian high (56.44%)

- Slight bullish bias maintained (52.99%)

### Practical Trading Applications

**Scenario 1: Range Projection**

If the ADR is 500 points and the market opens at 25,000:

- ADR High: 25,500 (potential resistance/target)

- ADR Low: 24,500 (potential support/target)

- Monitor how price interacts with these levels throughout the day

**Scenario 2: Session-Based Trading**

Using the statistics table, you notice London on Wednesdays averages 35 points. During a Wednesday London session:

- If London has already moved 30 points, the session may be exhausting its typical range

- If London has only moved 15 points with an hour remaining, there may be expansion potential

- Adjust stop losses and targets based on typical session behavior

**Scenario 3: Probability-Based Setup**

It's 8:05 AM ET and the indicator shows "London Partially Engulfs Upwards":

- You now know there's an 81.51% historical probability NY will take out London's high

- There's a 53.16% probability NY will reach down to Asia's low

- The NY Cash session has a slight bullish bias (55.52%)

- Consider this alongside your technical analysis for directional bias and level targeting

## Customization Options

### Visual Settings

- **Line Width**: Adjust thickness of ADR levels

- **ADR Color/Style**: Customize appearance of ADR projection lines (solid, dashed, dotted)

- **Median Line**: Toggle visibility and customize appearance separately

- **Session Box Colors**: Customize each session's box color independently

- **Show Session Boxes**: Toggle session box visibility on/off

### Label Settings

- **ADR Labels**: Show/hide labels for ADR High and ADR Low, adjust size

- **Median Label**: Separate control for median line label

- **Session Labels**: Show/hide session name labels, adjust size

- **Label Colors**: Customize text colors for all labels

### Table Settings

- **Session Stats Table**: Position (9 locations available), size (Tiny to Huge), toggle on/off

- **Sample Sizes**: Show/hide the number of historical samples used for each calculation

- **Probabilities Table**: Separate position and size controls, toggle on/off

### Session Times

- Each session's time range can be customized to fit different markets or preferences

- All times are in Eastern Time (America/New_York timezone)

## Technical Notes

### Data Requirements

- The indicator requires sufficient historical data based on your lookback settings

- Minimum recommended: 50+ days of intraday data for reliable statistics

- Works on any timeframe below Daily (1-minute, 5-minute, 15-minute, etc.)

### Calculation Methodology

- **ADR Calculation**: Simple average of absolute daily high-low ranges

- **Session Statistics**: Mean average of ranges for each session filtered by day of week

- **Condition Detection**: Boolean logic comparing session high/low relationships

- All calculations update in real-time as new bars form

### Probability Data Source

The probability statistics displayed in the dynamic table are derived from:

- **Dataset**: 12 years of NQ (Nasdaq E-mini futures) historical data

- **Methodology**: Frequency analysis of outcomes following specific setup conditions

- **Time Period**: Multiple market cycles including various volatility regimes

**Critical Warning**: These probabilities are specific to NQ and reflect that instrument's behavior patterns. Market microstructure, participant behavior, and volatility characteristics differ significantly across instruments. Do not apply these NQ-derived probabilities to other markets (ES, RTY, YM, individual stocks, forex, commodities, etc.).

## Best Practices

1. **Combine with Other Analysis**: Use this indicator as one component of a complete trading methodology, not a standalone system

2. **Respect Risk Management**: Probabilities are not certainties; always use proper position sizing and stop losses

3. **Context Matters**: High-impact news events, holiday trading, and extreme volatility can invalidate typical patterns

4. **Verify Statistics**: Monitor your own results and compare to the displayed probabilities

5. **Adapt Session Times**: If trading instruments with different active hours, adjust session times accordingly

6. **Regular Calibration**: Periodically review if the session averages and probabilities remain relevant to current market conditions

## Understanding Originality

This indicator is original in its approach to combining three analytical frameworks into a single tool:

1. **Dynamic ADR Projection**: Unlike static pivot points, these levels adapt daily based on recent volatility

2. **Session-Specific Statistics**: Goes beyond simple volume profiles by quantifying average ranges for specific time windows across weekdays

3. **Conditional Probability Display**: Automatically detects overnight session relationships and displays relevant probability data rather than showing all scenarios simultaneously

The conditional logic system that determines which probability set to display is a key differentiator—traders only see the statistics relevant to the current market setup, reducing information overload and improving decision-making clarity.

## Summary

The **Statistical Daily Profile & Ranges** indicator provides traders with a comprehensive framework for understanding daily range potential, session-specific behavior patterns, and probability-based setup analysis. By combining ADR projection levels with detailed session statistics and dynamic probability displays, traders gain multiple perspectives on potential price movement within the trading day.

The indicator is most effective when used to:

- Set realistic profit targets based on average daily range

- Identify which sessions typically produce movement on specific weekdays

- Understand probability-weighted outcomes for different overnight setup conditions (NQ only)

- Visualize session ranges and compare them to historical averages

Remember that all statistical analysis reflects historical patterns, and market behavior can change. Always combine indicator signals with sound risk management, proper position sizing, and your own market analysis.

Bar Statistics - DELTA/OI/TOTAL/BUY/SELL/LONGS/SHORTSBar Statistics - Advanced Volume & Open Interest Analysis

Overview

The Bar Statistics indicator is a comprehensive analytical tool designed to provide traders with detailed insights into market microstructure through advanced volume analysis, open interest tracking, and market flow detection. This indicator transforms complex market data into easily digestible visual information, displaying six key metrics in customizable colored boxes that update in real-time.

Unlike traditional volume indicators that only show basic volume data, this indicator combines multiple data sources to reveal the underlying forces driving price movement, including volume delta calculations from lower timeframes, open interest changes, and estimated market positioning.

What Makes This Indicator Unique

1. Multi-Timeframe Volume Delta Precision

The indicator utilizes lower timeframe data (default 1-second) to calculate highly accurate volume delta measurements, providing much more precise buy/sell pressure analysis than standard timeframe-based calculations. This approach captures intraday volume dynamics that are often missed by conventional indicators.

2. Real-Time Updates

Unlike many indicators that only update on bar completion, this tool provides live updates for the developing candle, allowing traders to see evolving market conditions as they happen.

3. Market Flow Analysis

The unique "L/S" (Long/Short) metric combines open interest changes with price/volume direction to estimate net market positioning, helping identify when participants are accumulating or distributing positions.

4. Adaptive Visual Intensity

The gradient color system automatically adjusts based on historical context, making it easy to identify when current values are significant relative to recent market activity.

5. Complete Customization

Every aspect of the display can be customized, from the order of metrics to individual color schemes, allowing traders to adapt the tool to their specific analysis needs.

6.All In One Solution

6 Metrics in one indicator no more using 5 different indicators.

Core Features Explained

DELTA (Volume Delta)

What it shows: Net difference between aggressive buy volume and aggressive sell volume

Calculation: Uses lower timeframe data to determine whether each trade was initiated by buyers or sellers

Interpretation:

Positive values indicate aggressive buying pressure

Negative values indicate aggressive selling pressure

Magnitude indicates the strength of directional pressure

OI Δ (Open Interest Change)

What it shows: Change in open interest from the previous bar

Data source: Fetches open interest data using the "_OI" symbol suffix

Interpretation:

Positive values indicate new positions entering the market

Negative values indicate positions being closed

Combined with price direction, reveals market participant behavior

L/S (Net Long/Short Bias)

What it shows: Estimated net change in long vs short market positions

Calculation method: Combines open interest changes with price/volume direction using configurable logic

Scenarios analyzed:

New Longs: Rising OI + Rising Price/Volume = Long position accumulation

Liquidated Longs: Falling OI + Falling Price/Volume = Long position exits

New Shorts: Rising OI + Falling Price/Volume = Short position accumulation

Covered Shorts: Falling OI + Rising Price/Volume = Short position exits

Result: Net bias toward long (positive) or short (negative) market sentiment

TOTAL (Total Volume)

What it shows: Standard volume for the current bar

Purpose: Provides context for other metrics and baseline activity measurement

Enhanced display: Uses gradient intensity based on recent volume history

BUY (Estimated Buy Volume)

What it shows: Estimated aggressive buy volume

Calculation: (Total Volume + Delta) / 2

Use case: Helps quantify the actual buying pressure in monetary/contract terms

SELL (Estimated Sell Volume)

What it shows: Estimated aggressive sell volume

Calculation: (Total Volume - Delta) / 2

Use case: Helps quantify the actual selling pressure in monetary/contract terms

Configuration Options

Timeframe Settings

Custom Timeframe Toggle: Enable/disable custom lower timeframe selection

Timeframe Selection: Choose the precision level for volume delta calculations

Auto-Selection Logic: Automatically selects optimal timeframe based on chart timeframe

Net Positions Calculation

Direction Method: Choose between Price-based or Volume Delta-based direction determination

Value Method: Select between Open Interest Change or Volume for position size calculations

Display Customization

Row Order: Completely customize which metrics appear and in what order (6 positions available)

Color Schemes: Individual color selection for positive/negative values of each metric

Gradient Intensity: Configurable lookback period (10-200 bars) for relative intensity calculations

Visual Elements

Box Format: Clean, professional box display with clear labels

Color Coding: Intuitive color schemes with customizable transparency gradients

Real-time Updates: Live updating for developing candles with historical stability

How to Use This Indicator

For Day Traders

Volume Confirmation: Use DELTA to confirm breakout validity - strong directional moves should show corresponding volume delta

Entry Timing: Watch for volume delta divergences at key levels to time entries

Exit Signals: Monitor when aggressive volume shifts against your position

For Swing Traders

Market Flow: Focus on the L/S metric to identify when participants are accumulating or distributing

Open Interest Analysis: Use OI Δ to confirm whether moves are backed by new money or position adjustments

Trend Validation: Combine multiple metrics to validate trend strength and sustainability

For Scalpers

Real-time Edge: Utilize the live updates to see developing imbalances before bar completion

Quick Decision Making: Focus on DELTA and BUY/SELL for immediate market pressure assessment

Volume Profile: Use TOTAL volume context for optimal entry/exit sizing

Setup Recommendations

Futures Markets: Enable OI tracking and use Volume Delta direction method

Crypto Markets: Focus on DELTA and volume metrics; OI may not be available

Stock Markets: Use Price direction method with volume value calculations

High-Frequency Analysis: Set lower timeframe to 1S for maximum precision

Technical Implementation

Data Accuracy

Utilizes TradingView's ta.requestVolumeDelta() function for precise buy/sell classification

Implements error checking for data availability

Handles missing data gracefully with fallback calculations

Performance Optimization

Efficient array management with configurable lookback periods

Smart box creation and deletion to prevent memory issues

Optimized real-time updates without historical data corruption

Compatibility

Works on all timeframes from seconds to daily

Compatible with futures, forex, crypto, and stock markets

Automatically adjusts calculation methods based on available data

Risk Disclaimers

This indicator is designed for educational and analytical purposes. It provides statistical analysis of market data but does not guarantee trading success. Users should:

Combine with other forms of analysis

Practice proper risk management

Understand that past performance doesn't predict future results

Be aware that volume delta and open interest data quality varies by market and data provider

Conclusion

The Bar Statistics indicator represents a significant advancement in retail trader access to professional-grade market analysis tools. By combining multiple data sources into a single, customizable display, it provides the depth of analysis needed for comprehensive market microstructure understanding while maintaining the simplicity required for effective decision-making.

Game Theory Trading StrategyGame Theory Trading Strategy: Explanation and Working Logic

This Pine Script (version 5) code implements a trading strategy named "Game Theory Trading Strategy" in TradingView. Unlike the previous indicator, this is a full-fledged strategy with automated entry/exit rules, risk management, and backtesting capabilities. It uses Game Theory principles to analyze market behavior, focusing on herd behavior, institutional flows, liquidity traps, and Nash equilibrium to generate buy (long) and sell (short) signals. Below, I'll explain the strategy's purpose, working logic, key components, and usage tips in detail.

1. General Description

Purpose: The strategy identifies high-probability trading opportunities by combining Game Theory concepts (herd behavior, contrarian signals, Nash equilibrium) with technical analysis (RSI, volume, momentum). It aims to exploit market inefficiencies caused by retail herd behavior, institutional flows, and liquidity traps. The strategy is designed for automated trading with defined risk management (stop-loss/take-profit) and position sizing based on market conditions.

Key Features:

Herd Behavior Detection: Identifies retail panic buying/selling using RSI and volume spikes.

Liquidity Traps: Detects stop-loss hunting zones where price breaks recent highs/lows but reverses.

Institutional Flow Analysis: Tracks high-volume institutional activity via Accumulation/Distribution and volume spikes.

Nash Equilibrium: Uses statistical price bands to assess whether the market is in equilibrium or deviated (overbought/oversold).

Risk Management: Configurable stop-loss (SL) and take-profit (TP) percentages, dynamic position sizing based on Game Theory (minimax principle).

Visualization: Displays Nash bands, signals, background colors, and two tables (Game Theory status and backtest results).

Backtesting: Tracks performance metrics like win rate, profit factor, max drawdown, and Sharpe ratio.

Strategy Settings:

Initial capital: $10,000.

Pyramiding: Up to 3 positions.

Position size: 10% of equity (default_qty_value=10).

Configurable inputs for RSI, volume, liquidity, institutional flow, Nash equilibrium, and risk management.

Warning: This is a strategy, not just an indicator. It executes trades automatically in TradingView's Strategy Tester. Always backtest thoroughly and use proper risk management before live trading.

2. Working Logic (Step by Step)

The strategy processes each bar (candle) to generate signals, manage positions, and update performance metrics. Here's how it works:

a. Input Parameters

The inputs are grouped for clarity:

Herd Behavior (🐑):

RSI Period (14): For overbought/oversold detection.

Volume MA Period (20): To calculate average volume for spike detection.

Herd Threshold (2.0): Volume multiplier for detecting herd activity.

Liquidity Analysis (💧):

Liquidity Lookback (50): Bars to check for recent highs/lows.

Liquidity Sensitivity (1.5): Volume multiplier for trap detection.

Institutional Flow (🏦):

Institutional Volume Multiplier (2.5): For detecting large volume spikes.

Institutional MA Period (21): For Accumulation/Distribution smoothing.

Nash Equilibrium (⚖️):

Nash Period (100): For calculating price mean and standard deviation.

Nash Deviation (0.02): Multiplier for equilibrium bands.

Risk Management (🛡️):

Use Stop-Loss (true): Enables SL at 2% below/above entry price.

Use Take-Profit (true): Enables TP at 5% above/below entry price.

b. Herd Behavior Detection

RSI (14): Checks for extreme conditions:

Overbought: RSI > 70 (potential herd buying).

Oversold: RSI < 30 (potential herd selling).

Volume Spike: Volume > SMA(20) x 2.0 (herd_threshold).

Momentum: Price change over 10 bars (close - close ) compared to its SMA(20).

Herd Signals:

Herd Buying: RSI > 70 + volume spike + positive momentum = Retail buying frenzy (red background).

Herd Selling: RSI < 30 + volume spike + negative momentum = Retail selling panic (green background).

c. Liquidity Trap Detection

Recent Highs/Lows: Calculated over 50 bars (liquidity_lookback).

Psychological Levels: Nearest round numbers (e.g., $100, $110) as potential stop-loss zones.

Trap Conditions:

Up Trap: Price breaks recent high, closes below it, with a volume spike (volume > SMA x 1.5).

Down Trap: Price breaks recent low, closes above it, with a volume spike.

Visualization: Traps are marked with small red/green crosses above/below bars.

d. Institutional Flow Analysis

Volume Check: Volume > SMA(20) x 2.5 (inst_volume_mult) = Institutional activity.

Accumulation/Distribution (AD):

Formula: ((close - low) - (high - close)) / (high - low) * volume, cumulated over time.

Smoothed with SMA(21) (inst_ma_length).

Accumulation: AD > MA + high volume = Institutions buying.

Distribution: AD < MA + high volume = Institutions selling.

Smart Money Index: (close - open) / (high - low) * volume, smoothed with SMA(20). Positive = Smart money buying.

e. Nash Equilibrium

Calculation:

Price mean: SMA(100) (nash_period).

Standard deviation: stdev(100).

Upper Nash: Mean + StdDev x 0.02 (nash_deviation).

Lower Nash: Mean - StdDev x 0.02.

Conditions:

Near Equilibrium: Price between upper and lower Nash bands (stable market).

Above Nash: Price > upper band (overbought, sell potential).

Below Nash: Price < lower band (oversold, buy potential).

Visualization: Orange line (mean), red/green lines (upper/lower bands).

f. Game Theory Signals

The strategy generates three types of signals, combined into long/short triggers:

Contrarian Signals:

Buy: Herd selling + (accumulation or down trap) = Go against retail panic.

Sell: Herd buying + (distribution or up trap).

Momentum Signals:

Buy: Below Nash + positive smart money + no herd buying.

Sell: Above Nash + negative smart money + no herd selling.

Nash Reversion Signals:

Buy: Below Nash + rising close (close > close ) + volume > MA.

Sell: Above Nash + falling close + volume > MA.

Final Signals:

Long Signal: Contrarian buy OR momentum buy OR Nash reversion buy.

Short Signal: Contrarian sell OR momentum sell OR Nash reversion sell.

g. Position Management

Position Sizing (Minimax Principle):

Default: 1.0 (10% of equity).

In Nash equilibrium: Reduced to 0.5 (conservative).

During institutional volume: Increased to 1.5 (aggressive).

Entries:

Long: If long_signal is true and no existing long position (strategy.position_size <= 0).

Short: If short_signal is true and no existing short position (strategy.position_size >= 0).

Exits:

Stop-Loss: If use_sl=true, set at 2% below/above entry price.

Take-Profit: If use_tp=true, set at 5% above/below entry price.

Pyramiding: Up to 3 concurrent positions allowed.

h. Visualization

Nash Bands: Orange (mean), red (upper), green (lower).

Background Colors:

Herd buying: Red (90% transparency).

Herd selling: Green.

Institutional volume: Blue.

Signals:

Contrarian buy/sell: Green/red triangles below/above bars.

Liquidity traps: Red/green crosses above/below bars.

Tables:

Game Theory Table (Top-Right):

Herd Behavior: Buying frenzy, selling panic, or normal.

Institutional Flow: Accumulation, distribution, or neutral.

Nash Equilibrium: In equilibrium, above, or below.

Liquidity Status: Trap detected or safe.

Position Suggestion: Long (green), Short (red), or Wait (gray).

Backtest Table (Bottom-Right):

Total Trades: Number of closed trades.

Win Rate: Percentage of winning trades.

Net Profit/Loss: In USD, colored green/red.

Profit Factor: Gross profit / gross loss.

Max Drawdown: Peak-to-trough equity drop (%).

Win/Loss Trades: Number of winning/losing trades.

Risk/Reward Ratio: Simplified Sharpe ratio (returns / drawdown).

Avg Win/Loss Ratio: Average win per trade / average loss per trade.

Last Update: Current time.

i. Backtesting Metrics

Tracks:

Total trades, winning/losing trades.

Win rate (%).

Net profit ($).

Profit factor (gross profit / gross loss).

Max drawdown (%).

Simplified Sharpe ratio (returns / drawdown).

Average win/loss ratio.

Updates metrics on each closed trade.

Displays a label on the last bar with backtest period, total trades, win rate, and net profit.

j. Alerts

No explicit alertconditions defined, but you can add them for long_signal and short_signal (e.g., alertcondition(long_signal, "GT Long Entry", "Long Signal Detected!")).

Use TradingView's alert system with Strategy Tester outputs.

3. Usage Tips

Timeframe: Best for H1-D1 timeframes. Shorter frames (M1-M15) may produce noisy signals.

Settings:

Risk Management: Adjust sl_percent (e.g., 1% for volatile markets) and tp_percent (e.g., 3% for scalping).

Herd Threshold: Increase to 2.5 for stricter herd detection in choppy markets.

Liquidity Lookback: Reduce to 20 for faster markets (e.g., crypto).

Nash Period: Increase to 200 for longer-term analysis.

Backtesting:

Use TradingView's Strategy Tester to evaluate performance.

Check win rate (>50%), profit factor (>1.5), and max drawdown (<20%) for viability.

Test on different assets/timeframes to ensure robustness.

Live Trading:

Start with a demo account.

Combine with other indicators (e.g., EMAs, support/resistance) for confirmation.

Monitor liquidity traps and institutional flow for context.

Risk Management:

Always use SL/TP to limit losses.

Adjust position_size for risk tolerance (e.g., 5% of equity for conservative trading).

Avoid over-leveraging (pyramiding=3 can amplify risk).

Troubleshooting:

If no trades are executed, check signal conditions (e.g., lower herd_threshold or liquidity_sensitivity).

Ensure sufficient historical data for Nash and liquidity calculations.

If tables overlap, adjust position.top_right/bottom_right coordinates.

4. Key Differences from the Previous Indicator

Indicator vs. Strategy: The previous code was an indicator (VP + Game Theory Integrated Strategy) focused on visualization and alerts. This is a strategy with automated entries/exits and backtesting.

Volume Profile: Absent in this strategy, making it lighter but less focused on high-volume zones.

Wick Analysis: Not included here, unlike the previous indicator's heavy reliance on wick patterns.

Backtesting: This strategy includes detailed performance metrics and a backtest table, absent in the indicator.

Simpler Signals: Focuses on Game Theory signals (contrarian, momentum, Nash reversion) without the "Power/Ultra Power" hierarchy.

Risk Management: Explicit SL/TP and dynamic position sizing, not present in the indicator.

5. Conclusion

The "Game Theory Trading Strategy" is a sophisticated system leveraging herd behavior, institutional flows, liquidity traps, and Nash equilibrium to trade market inefficiencies. It’s designed for traders who understand Game Theory principles and want automated execution with robust risk management. However, it requires thorough backtesting and parameter optimization for specific markets (e.g., forex, crypto, stocks). The backtest table and visual aids make it easy to monitor performance, but always combine with other analysis tools and proper capital management.

If you need help with backtesting, adding alerts, or optimizing parameters, let me know!

Liquidity Break Probability [PhenLabs]📊 Liquidity Break Probability

Version: PineScript™ v6

The Liquidity Break Probability indicator revolutionizes how traders approach liquidity levels by providing real-time probability calculations for level breaks. This advanced indicator combines sophisticated market analysis with machine learning inspired probability models to predict the likelihood of high/low breaks before they happen.

Unlike traditional liquidity indicators that simply draw lines, LBP analyzes market structure, volume profiles, momentum, volatility, and sentiment to generate dynamic break probabilities ranging from 5% to 95%. This gives traders unprecedented insight into which levels are most likely to hold or break, enabling more confident trading decisions.

🚀 Points of Innovation

Advanced 6-factor probability model weighing market structure, volatility, volume, momentum, patterns, and sentiment

Real-time probability updates that adjust as market conditions change

Intelligent trading style presets (Scalping, Day Trading, Swing Trading) with optimized parameters

Dynamic color-coded probability labels showing break likelihood percentages

Professional tiered input system - from quick setup to expert-level customization

Smart volume filtering that only highlights levels with significant institutional interest

🔧 Core Components

Market Structure Analysis: Evaluates trend alignment, level strength, and momentum buildup using EMA crossovers and price action

Volatility Engine: Incorporates ATR expansion, Bollinger Band positioning, and price distance calculations

Volume Profile System: Analyzes current volume strength, smart money proxies, and level creation volume ratios

Momentum Calculator: Combines RSI positioning, MACD strength, and momentum divergence detection

Pattern Recognition: Identifies reversal patterns (doji, hammer, engulfing) near key levels

Sentiment Analysis: Processes fear/greed indicators and market breadth measurements

🔥 Key Features

Dynamic Probability Labels: Real-time percentage displays showing break probability with color coding (red >70%, orange >50%, white <50%)

Trading Style Optimization: One-click presets automatically configure sensitivity and parameters for your trading timeframe

Professional Dashboard: Live market state monitoring with nearest level tracking and active level counts

Smart Alert System: Customizable proximity alerts and high-probability break notifications

Advanced Level Management: Intelligent line cleanup and historical analysis options

Volume-Validated Levels: Only displays levels backed by significant volume for institutional-grade analysis

🎨 Visualization

Recent Low Lines: Red lines marking validated support levels with probability percentages

Recent High Lines: Blue lines showing resistance zones with break likelihood indicators

Probability Labels: Color-coded percentage labels that update in real-time

Professional Dashboard: Customizable panel showing market state, active levels, and current price

Clean Display Modes: Toggle between active-only view for clean charts or historical view for analysis

📖 Usage Guidelines

Quick Setup

Trading Style Preset

Default: Day Trading

Options: Scalping, Day Trading, Swing Trading, Custom

Description: Automatically optimizes all parameters for your preferred trading timeframe and style

Show Break Probability %

Default: True

Description: Displays percentage labels next to each level showing break probability

Line Display

Default: Active Only

Options: Active Only, All Levels

Description: Choose between clean active-only view or comprehensive historical analysis

Level Detection Settings

Level Sensitivity

Default: 5

Range: 1-20

Description: Lower values show more levels (sensitive), higher values show fewer levels (selective)

Volume Filter Strength

Default: 2.0

Range: 0.5-5.0

Description: Controls minimum volume threshold for level validation

Advanced Probability Model

Market Trend Influence

Default: 25%

Range: 0-50%

Description: Weight given to overall market trend in probability calculations

Volume Influence

Default: 20%

Range: 0-50%

Description: Impact of volume analysis on break probability

✅ Best Use Cases

Identifying high-probability breakout setups before they occur

Determining optimal entry and exit points near key levels

Risk management through probability-based position sizing

Confluence trading when multiple high-probability levels align

Scalping opportunities at levels with low break probability

Swing trading setups using high-probability level breaks

⚠️ Limitations

Probability calculations are estimations based on historical patterns and current market conditions

High-probability setups do not guarantee successful trades - risk management is essential

Performance may vary significantly across different market conditions and asset classes

Requires understanding of support/resistance concepts and probability-based trading

Best used in conjunction with other analysis methods and proper risk management

💡 What Makes This Unique

Probability-Based Approach: First indicator to provide quantitative break probabilities rather than simple S/R lines

Multi-Factor Analysis: Combines 6 different market factors into a comprehensive probability model

Adaptive Intelligence: Probabilities update in real-time as market conditions change

Professional Interface: Tiered input system from beginner-friendly to expert-level customization

Institutional-Grade Filtering: Volume validation ensures only significant levels are displayed

🔬 How It Works

1. Level Detection:

Identifies pivot highs and lows using configurable sensitivity settings

Validates levels with volume analysis to ensure institutional significance

2. Probability Calculation:

Analyzes 6 key market factors: structure, volatility, volume, momentum, patterns, sentiment

Applies weighted scoring system based on user-defined factor importance

Generates probability score from 5% to 95% for each level

3. Real-Time Updates:

Continuously monitors price action and market conditions

Updates probability calculations as new data becomes available

Adjusts for level touches and changing market dynamics

💡 Note: This indicator works best on timeframes from 1-minute to 4-hour charts. For optimal results, combine with proper risk management and consider multiple timeframe analysis. The probability calculations are most accurate in trending markets with normal to high volatility conditions.

SMC Liquidity Engine Pro SMC Liquidity Engine Pro - Complete Trading Guide & Documentation

📊 Introduction: Understanding Smart Money Concepts

The SMC Liquidity Engine Pro is a comprehensive, institutional-grade trading indicator that brings professional Smart Money Concepts (SMC) methodology directly to your TradingView charts. This isn't just another technical indicator—it's a complete framework for understanding how institutional traders, market makers, banks, and hedge funds manipulate and move the markets.

What Makes This Different?

While most retail traders rely on lagging indicators like moving averages or RSI, this indicator reveals the real-time footprints of institutional activity. It shows you:

Where large players are accumulating or distributing positions

How they engineer liquidity to trigger retail stop losses

When they're shifting from one directional bias to another

Where price inefficiencies exist that institutions will likely revisit

The markets don't move randomly—they move based on liquidity. Understanding this fundamental truth is what separates consistently profitable traders from those who struggle. This indicator decodes that liquidity-driven behavior and presents it in clear, actionable visual signals.

The Philosophy Behind Smart Money Concepts

Smart Money Concepts is built on several core principles:

1. Liquidity is King: Price doesn't move because of patterns or indicators—it moves to collect liquidity (stop losses and pending orders). Institutions need massive liquidity to fill their large positions, so they engineer price movements to create that liquidity before making their real directional move.

2. Market Structure Reveals Intent: The way price forms highs and lows tells a story about who's in control. When structure breaks, it signals a shift in institutional positioning.

3. Inefficiencies Get Filled: When price moves too quickly in one direction, it leaves behind "fair value gaps"—areas of imbalance. Institutions frequently return to these areas to fill orders and restore balance.

4. Manipulation Precedes True Moves: The most explosive directional moves are often preceded by liquidity sweeps in the opposite direction—trapping retail traders before the real move begins.

This indicator automates the identification of all these concepts, allowing you to trade alongside the smart money rather than being their exit liquidity.

🎯 Core Features - Deep Dive

1. Market Structure Detection & Visualization

What It Is: Market structure forms the foundation of all Smart Money analysis. This indicator automatically identifies and tracks swing highs and swing lows using a sophisticated pivot detection algorithm. These aren't just any price points—they represent areas where the market showed a significant shift in supply and demand dynamics.

How It Works: The indicator uses a customizable lookback period to identify valid swing points. A swing high must have lower highs on both sides within the lookback period, and a swing low must have higher lows on both sides. This ensures that only significant structural points are marked, filtering out minor noise and consolidation.

Visual Presentation:

Bullish Structure (Cyan Lines): Horizontal lines extending from each identified swing high, showing resistance levels that price previously respected

Bearish Structure (Red Lines): Horizontal lines extending from each identified swing low, showing support levels where buying pressure emerged

Trading Application: These structure levels serve multiple purposes:

Target Zones: Previous highs become targets in uptrends; previous lows become targets in downtrends

Invalidation Levels: If expecting a bullish move, breaking below the last swing low invalidates the setup

Context for Other Signals: All BOS, CHOCH, and liquidity sweep signals gain meaning from their relationship to structure

Multi-Timeframe Anchors: Higher timeframe structure provides context for lower timeframe entries

Advanced Tip: When multiple timeframe structures align (e.g., a daily swing low coincides with a 4-hour swing low), these levels carry significantly more weight and are more likely to be defended or, when broken, lead to explosive moves.

2. Break of Structure (BOS) - Trend Confirmation

What It Is: A Break of Structure occurs when price definitively closes beyond a previous swing high (bullish BOS) or swing low (bearish BOS). This signals that the current trend maintains its momentum and is likely to continue in the same direction.

The Institutional Perspective: When institutions want to continue pushing price in a direction, they need to break through previous resistance or support. A clean BOS indicates that:

There's sufficient institutional buying/selling to overcome the supply/demand at previous structure

The trend has enough momentum to attract more participants

Stop losses above/below structure have been triggered, providing liquidity for continuation

Signal Characteristics:

Bullish BOS Label: Appears below the bar that closes above the previous swing high

Bearish BOS Label: Appears above the bar that closes below the previous swing low

Confirmation: Requires a full candle close, preventing false signals from wicks

Trading Strategies:

Trend Continuation Entries: After a BOS, wait for a pullback to a Fair Value Gap or minor structure, then enter in the direction of the break

Breakout Trading: Enter immediately on BOS confirmation with a stop below the broken structure

Momentum Confirmation: Use BOS to confirm that your existing position is aligned with institutional flow

Scaling Strategy: Add to positions on each successive BOS in trending markets

What to Watch For:

Volume: Strong BOS movements should be accompanied by above-average volume

Speed: Rapid price movement through structure suggests institutional urgency

Follow-Through: The best BOS signals see price continue strongly without immediately reversing

Higher Timeframe Alignment: BOS on higher timeframes (4H, Daily) carry more weight than lower timeframe breaks

Common Pitfalls:

Not all structure breaks are equal—BOS during ranging markets are less reliable

A BOS immediately followed by a reversal back into the range may indicate a failed breakout

During major news events, structure can be broken temporarily without institutional intent

3. Liquidity Sweep Detection - Spotting Manipulation

What It Is: Liquidity sweeps (also called "stop hunts" or "liquidity grabs") occur when price temporarily breaks beyond a key level to trigger stop losses and pending orders, then immediately reverses back. This is one of the most important concepts in SMC trading because it reveals intentional manipulation.

Why Institutions Do This: Large institutional orders can't be filled at a single price point—they need massive liquidity. The biggest pools of liquidity sit just beyond obvious highs and lows where retail traders place their stops. By briefly pushing price into these zones, institutions:

Trigger retail stop losses (creating market orders)

Activate pending buy/sell orders

Fill their large positions at favorable prices

Trap late breakout traders before reversing

Detection Methodology: The indicator identifies sweeps using multiple criteria:

Price must penetrate beyond the structural high/low (creating the sweep)

The candle must close back on the opposite side of the structure (confirming rejection)

The sweep distance is measured against ATR to distinguish manipulation from normal volatility

The sweep multiplier setting allows you to adjust sensitivity based on market conditions

Visual Indicators:

Orange Down Arrows: Mark liquidity sweeps above structural highs

Lime Up Arrows: Mark liquidity sweeps below structural lows

Liquidity Zone Boxes: Semi-transparent colored boxes highlight the exact range of the swept area

Persistent Display: Zones remain visible for several bars to maintain context

Trading Applications:

Reversal Trading: Liquidity sweeps often mark excellent reversal points. After a sweep:

Wait for the sweep to complete (candle closes back inside structure)

Look for a Change of Character signal for confirmation

Enter in the direction opposite to the sweep

Place stops beyond the sweep high/low

Target the opposite side of the range or next structural level

Continuation Filtering: Not all sweeps lead to reversals. During strong trends:

Sweeps of minor structure in a trending market often precede continuation

Use higher timeframe structure to determine if a sweep is counter-trend (likely reversal) or with-trend (likely continuation)

Entry Refinement: In ranging markets, trade from swept lows to highs and vice versa, as institutions accumulate at the extremes.

Advanced Sweep Analysis:

Double Sweeps: When both sides of a range are swept, expect a strong breakout

Sweep Rejection Quality: Fast, strong rejections of sweeps are more reliable than slow grinding returns

Timeframe Consideration: Daily timeframe sweeps are significantly more important than 15-minute sweeps

Volume Profile: Sweeps with low volume followed by high volume reversals confirm manipulation

What Makes a High-Quality Sweep Signal: ✅ Penetrates structure by at least 0.5-1x ATR

✅ Strong rejection candle (long wick, decisive close)

✅ Occurs at a higher timeframe structural level

✅ Creates a Change of Character on the following move

✅ Sweeps an obvious level where retail stops cluster

4. Change of Character (CHOCH) - Major Reversal Signals

What It Is: A Change of Character represents the most significant shift in market dynamics—when the entire structural bias of the market flips from bullish to bearish or bearish to bullish. CHOCH signals are the crown jewel of SMC trading because they identify the exact moment when institutional positioning fundamentally changes.

The Anatomy of a CHOCH: A valid CHOCH requires a specific sequence:

Established Trend: A clear directional bias with multiple BOS in one direction

Liquidity Engineering: A sweep of structure in the current trend direction (the manipulation phase)

Structural Break: Price then breaks structure in the OPPOSITE direction (the revelation phase)

This combination shows that institutions have:

Completed their accumulation/distribution at favorable prices (via the sweep)

Shifted their positioning from bullish to bearish (or vice versa)

Begun a new directional campaign

Visual Presentation:

Bullish CHOCH (Cyan Triangle Up): Appears when bearish structure is broken after a low sweep, signaling the shift to bullish control

Bearish CHOCH (Red Triangle Down): Appears when bullish structure is broken after a high sweep, signaling the shift to bearish control

Prominent Markers: Larger and more visually distinct than BOS signals, reflecting their importance

Why CHOCH Signals Are So Powerful:

Trend Reversal Identification: They mark the earliest possible confirmation of a trend change

High Win Rate: When combined with proper risk management, CHOCH signals have among the highest success rates in SMC trading

Risk-Reward Ratio: Entering at CHOCH gives you the best possible risk-reward since you're entering at the beginning of a new trend

Institutional Confirmation: The sequence of sweep + structure break proves institutional repositioning, not just retail sentiment

Trading CHOCH Signals:

The Perfect CHOCH Setup:

Identify the Sweep: Watch for a liquidity sweep of structural lows (for bullish) or highs (for bearish)

Wait for the Break: Don't enter on the sweep—wait for structure to break in the opposite direction

CHOCH Confirmation: The indicator fires the CHOCH signal—this is your entry trigger

Entry Execution:

Aggressive: Enter immediately on CHOCH confirmation

Conservative: Wait for a pullback to the first Fair Value Gap or broken structure (now turned support/resistance)

Stop Placement: Beyond the swept liquidity point

Target Selection: Previous swing in the opposite direction, or let it run to the next CHOCH

Multiple Timeframe CHOCH Strategy: The most powerful setups occur when CHOCHs align across timeframes:

Daily CHOCH: Signals major institutional trend change, target 500+ pips (Forex) or significant point moves

4H CHOCH: Confirms daily direction, provides swing trade opportunities

1H CHOCH: Offers precise entry timing within the higher timeframe trend

15M CHOCH: Used for position scaling and intraday management

Example Trade Flow:

Daily Chart: Bullish CHOCH appears after weeks of downtrend

↓

4H Chart: Wait for pullback after the daily CHOCH, then catch the 4H bullish CHOCH

↓

1H Chart: Enter on the 1H bullish CHOCH that aligns with both higher timeframes

↓

Result: You've entered at the beginning of a major trend with multiple confirmations

CHOCH Quality Grading:

A-Grade CHOCH (Highest Probability):

Occurs at major higher timeframe structure

Following a clear liquidity sweep

Volume spike on the structural break

Multiple timeframe alignment

Creates a large Fair Value Gap on the break

B-Grade CHOCH (Good Probability):

Valid sweep and structure break

Single timeframe signal

Moderate volume

Occurs at minor structure

C-Grade CHOCH (Lower Probability):

Choppy, ranging market context

Weak sweep or unclear structure

Counter to higher timeframe trend

Low volume confirmation

Common Mistakes with CHOCH Trading: ❌ Entering on the sweep instead of waiting for the structure break

❌ Ignoring higher timeframe context

❌ Taking every CHOCH regardless of quality

❌ Not waiting for pullbacks on aggressive trends

❌ Placing stops too tight, getting caught in volatility

Advanced CHOCH Concepts:

Failed CHOCH: Occasionally, what appears to be a CHOCH will fail (price reverses back into the previous trend). This often indicates:

Insufficient institutional conviction for the reversal

Fake-out to grab liquidity in the opposite direction

Need to wait for a higher timeframe CHOCH for confirmation

When a CHOCH fails, it often sets up an even stronger continuation of the original trend.

CHOCH vs BOS Decision Matrix:

If in doubt about trend direction → wait for CHOCH

If confident in trend → trade BOS continuations

After a CHOCH → next signals in the new direction are BOS

5. Fair Value Gaps (FVG) - Institutional Retracement Zones

What It Is: Fair Value Gaps represent price imbalances where the market moved so quickly that it left behind inefficient pricing. These gaps form when there's no overlap between the current candle's wick and the candle from two bars ago—a void in the price action that creates a "gap" in the order flow.

The Institutional Logic: When institutions execute large market orders, they can push price rapidly through levels without allowing normal two-way trading. This creates unfilled orders and imbalanced order books. Institutions often return to these gaps to:

Fill additional orders at more favorable prices

Allow the market to "breathe" before the next push

Create support/resistance at the gap for the next move

Restore balance to the order book

FVG Formation Criteria: This indicator uses enhanced FVG detection logic:

Bullish FVG (Upward Gap):

Current candle's low is above the high from 2 candles ago

Creates a visible gap where no trading occurred

Gap size must exceed 30% of ATR (filtering minor gaps)

Typically forms on strong bullish momentum candles

Market moved up so fast it left unfilled sell orders

Bearish FVG (Downward Gap):

Current candle's high is below the low from 2 candles ago

Creates a visible gap where no trading occurred

Gap size must exceed 30% of ATR

Typically forms on strong bearish momentum candles

Market moved down so fast it left unfilled buy orders

Visual Presentation:

Bullish FVG Zones: Semi-transparent cyan boxes extending from gap bottom to top

Bearish FVG Zones: Semi-transparent red boxes extending from gap top to bottom

Dynamic Management: Gaps automatically removed when filled or expired

Clean Display: Only active, unfilled gaps shown to prevent chart clutter

FVG Trading Strategies:

Strategy 1: FVG Retracement Entries After a CHOCH or strong BOS, wait for price to retrace into the FVG for entry:

Identify trend direction via CHOCH or BOS

Locate the nearest FVG in the direction of the trend

Set limit orders within the FVG zone

Stop loss beyond the FVG

Target the next structural level or previous swing

Strategy 2: FVG Breakout Confirmation When price breaks through an FVG without filling it:

Signals extreme institutional urgency

Indicates the move is likely to continue strongly

The unfilled gap becomes a "no-go zone" for counter-trend entries

Strategy 3: Multiple FVG Management When multiple FVGs form in sequence:

The first FVG is most likely to be filled

If price skips the first FVG, it signals exceptional strength

Sequential gaps create a "gap ladder" for scaling into positions

FVG Quality Assessment:

High-Quality FVGs (Best Trading Zones):

Large gap size (1.5x+ ATR)

Formed on high volume impulse moves

Aligned with higher timeframe structure

Created during CHOCH or strong BOS

Positioned between current price and key structure

Low-Quality FVGs (Use Caution):

Small gaps (< 0.5 ATR)

Formed during choppy, ranging conditions

Multiple overlapping gaps in the same area

Counter to higher timeframe trend

Very old gaps (50+ bars ago)

FVG Lifecycle Management:

The indicator intelligently manages FVG zones:

Gap Filling:

Bullish FVG is "filled" when price touches the bottom of the gap

Bearish FVG is "filled" when price touches the top of the gap

Filled gaps are automatically removed from the chart

Partial fills count as complete fills (institutions got their orders)

Gap Expiration:

Gaps older than the extension period (default 10 bars) are removed

This keeps the chart clean and focuses on relevant levels

Adjustable from 5-50 bars based on timeframe and trading style

Gap Priority: When multiple gaps exist, closest gap to current price is most relevant

Advanced FVG Concepts:

Nested FVGs: Sometimes FVGs form within larger FVGs. The smaller, more recent gap typically gets filled first, providing a secondary entry within the larger gap.

FVG Clusters: When 3+ FVGs stack in the same zone, this area becomes a major institutional reaccumulation zone—excellent for swing entries.

Inverted FVGs: Bullish FVGs in downtrends or bearish FVGs in uptrends can act as resistance/support where rallies/dips fail.

FVG + Liquidity Sweep Combination: The ultimate entry setup:

Liquidity sweep occurs

CHOCH confirms reversal

Price retraces into FVG created during the CHOCH move

Enter with exceptional risk-reward ratio

FVG Statistics & Probabilities:

Research on FVG behavior shows:

Approximately 70% of FVGs get filled within 20 bars

FVGs formed during CHOCH have 80%+ fill rate

Larger gaps (2x+ ATR) have lower but higher-quality fill rates

Higher timeframe FVGs are more magnetic than lower timeframe

Timeframe Considerations:

Daily FVGs:

Can remain unfilled for weeks

Major institutional zones

Often mark the absolute best entry prices for swing trades

When filled, usually result in strong reactions

4H FVGs:

Typically fill within 3-7 days

Excellent for swing trading

Balance between frequency and reliability

1H FVGs:

Usually fill within 1-3 days

Good for short-term position trading

More frequent signals

15M FVGs:

Often fill same day

Best used for intraday refinement

Should align with higher timeframe gaps

🔧 Customization & Settings Guide

Structure Detection Settings

Swing Lookback Period (3-50 bars): This is arguably the most important setting as it determines what the indicator considers "structure."

Low Values (3-7):

Identifies minor swings and frequent structure points

More BOS and CHOCH signals

Better for scalping and day trading

Risk: More false signals in choppy markets

Best for: 15M-1H charts, active traders

Medium Values (8-15):

Balanced approach capturing meaningful swings

Default setting works well for most traders

Good signal-to-noise ratio

Best for: 1H-4H charts, swing traders

High Values (16-50):

Only major structural points identified

Fewer but higher-quality signals

Cleaner charts with less noise

Better for trending markets

Best for: 4H-Daily charts, position traders

ATR Period (1-50): Controls how volatility is measured for liquidity sweep detection.

Shorter Periods (7-14):

More responsive to recent volatility changes

Better during high volatility events

May overreact to short-term spikes

Longer Periods (15-30):

Smoother, more stable volatility measurement

Better for swing trading

Reduces sensitivity to short-term noise

Liquidity Sweep Multiplier (0.5-3.0): Determines how far beyond structure price must move to qualify as a sweep.

Low Multiplier (0.5-0.9):

Catches smaller, more frequent sweeps

More signals but lower reliability

Good for scalping or high-frequency trading

Use in ranging markets

Medium Multiplier (1.0-1.5):

Balanced sensitivity

Default 1.2 works for most situations

Good signal quality

High Multiplier (1.6-3.0):

Only major, obvious sweeps detected

Fewer but very high-quality signals

Best for trending markets

Use when you want only the clearest setups

Display Options

Toggle Controls: Each component can be individually enabled/disabled:

Show Market Structure:

Turn off when chart becomes too cluttered

Essential for understanding context, generally keep ON

Disable only when you know structure from higher timeframe

Show Liquidity Zones:

Highlights swept areas with boxes

Can be disabled if you prefer cleaner charts

Keep ON when learning to spot manipulation

Show Break of Structure:

BOS labels can be disabled if trading only reversals

Keep ON for trend following strategies

Show Change of Character:

Core SMC signal, usually keep ON

Only disable if focusing purely on continuation trading

Show Fair Value Gaps:

OFF by default to prevent overwhelming new users

Turn ON once comfortable with basic structure

Can generate many zones on lower timeframes

FVG Extension Period (5-50 bars): Determines how long unfilled gaps remain displayed.

Short Extension (5-10):

Keeps charts very clean

Only shows very recent gaps

Good for day trading

May remove gaps before they fill

Medium Extension (11-25):

Balanced approach

Captures most gap fills

Good for swing trading

Long Extension (26-50):

Shows historical gap context

Better for position trading

Higher timeframe analysis

Can make charts busy on lower timeframes

Color Scheme Customization

Why Colors Matter: Visual clarity is crucial for quick decision-making. The color scheme should:

Clearly distinguish bullish vs bearish elements

Work well with your chart background (dark/light mode)

Be visible but not distracting

Match your personal preference for aesthetics

Default Colors:

Bullish: Cyan (

#00ffff) - visibility and association with "cool" buying

Bearish: Red (

#ff0051) - visibility and universal danger/selling association

FVG Bullish: 85% transparent cyan - visible but not overpowering

FVG Bearish: 85% transparent red - visible but not overpowering

Customization Tips:

Increase transparency if zones overwhelm price action

Use higher contrast colors on light backgrounds

Keep bullish/bearish colors visually distinct

Test colors across different market conditions

Optimization by Market Type

Forex (24-hour markets):

Structure Lookback: 10-15

ATR Period: 14-21

Sweep Multiplier: 1.0-1.5

Best Timeframes: 15M, 1H, 4H

Stocks (Session-based):

Structure Lookback: 8-12

ATR Period: 14

Sweep Multiplier: 1.2-1.8

Best Timeframes: 5M, 15M, 1H, Daily

Note: Gaps at market open/close aren't FVGs

Cryptocurrency (High volatility):

Structure Lookback: 12-20 (filter noise)

ATR Period: 10-14 (responsive to volatility)

Sweep Multiplier: 1.5-2.5 (larger sweeps)

Best Timeframes: 15M, 1H, 4H

Indices (Moderate volatility):

Structure Lookback: 10-15

ATR Period: 14-20

Sweep Multiplier: 1.0-1.5

Best Timeframes: 1H, 4H, Daily

📈 Complete Trading System & Strategies

The Complete SMC Trading Process

Step 1: Higher Timeframe Analysis (Daily/4H) Begin every trading session by analyzing higher timeframes:

Identify the prevailing market structure (bullish or bearish)

Mark key swing highs and lows

Note any recent CHOCHs that signal trend changes

Identify major Fair Value Gaps that could act as targets or entry zones

Determine areas of liquidity (obvious highs/lows where stops cluster)

Step 2: Trading Timeframe Setup (1H/4H) Move to your primary trading timeframe:

Wait for alignment with higher timeframe bias

Look for CHOCH signals if expecting reversal

Look for BOS signals if expecting continuation

Identify liquidity sweeps that create trading opportunities

Note nearby FVGs for entry refinement